The Dollar’s Second Life

Once dismissed as a systemic risk to crypto, stablecoins are now centre stage in global finance. I wrote this piece for Hedge News Africa to explain what changed - and why it matters. This is one of the most consequential shifts happening in money right now. Here’s what you need to know.

Conclusions:

The GENIUS Act has regulated stablecoins in the same way as money market funds in the US

The US government needs stablecoins to purchase its debt

Stablecoins provide another bridge into non-state crypto assets, like bitcoin

Most banks and payments providers will settle in stablecoins in 5 year’s time

Equity markets will follow the dollars tokenisation trend, trading 24/7 peer to peer

Forex markets will consolidate towards USD & Bitcoin, with many Emerging Market currencies fading into irrelevance

Stablecoins were born as a workaround – arguably even a workaround to the law. A shadow-dollar system for crypto traders when banks wouldn’t touch them. For years, Tether – and by extension, the entire stablecoin sector – was viewed by many as a Ponzi scheme, one of the biggest existential risks to crypto markets. From its early days as an offshore dollar settlement tool for crypto exchanges, with longstanding doubts around its reserves and a string of US court cases, Tether carried a heavy dose of scepticism. And who could forget the spectacular collapse of Terra’s UST – an “algorithmic stablecoin” – which wiped out billions in investor capital overnight in 2022.

Yet here we are in 2025, and the GENIUS Act has just been signed into law – greenlighting regulated stablecoins in the US, in what could be the most consequential financial regulation since Dodd-Frank. The US government has quietly realised: they need stablecoins. To soak up the debt. To defend dollar dominance. Stablecoins have become one of the fastest-growing areas of modern finance, and they are dominated by US dollars. Financial giants are practically frothing at the mouth to issue their own, or to offer infrastructure and custody services to this new monetary layer.

It’s a remarkable reversal. Born in the shadows, stablecoins are now being hardwired into the mainstream. The technology could reshape everything from global currency markets and cross-border payments, creating new adoption pathways for non- state decentralised crypto assets like bitcoin.

Built for traders, hijacked by the world

Crypto traders had a problem in the mid- 2010s: Bitcoin traded 24/7, but banks didn’t. They needed a way to take profits into dollars – without waiting for Monday.

Enter stablecoins: dollars on crypto rails. They enable a version of the dollar that’s global, frictionless, and always on. No closing bell, no bank holidays. More than just a trading convenience, stablecoins function like digital cash. They allow peer-to-peer payments across borders, with the speed and openness of the internet, which is a particularly interesting quality at a time when physical cash is moving out of circulation.

While the US dollar is clearly the global reserve currency, it is difficult, costly and time-consuming to send capital across the globe, and it requires numerous intermediaries. Almost anyone with an internet connection can open a stablecoin wallet and start receiving/sending capital from/ to anyone/anywhere in minutes. Plus, transactions settle almost instantly without intermediaries. That’s powerful!

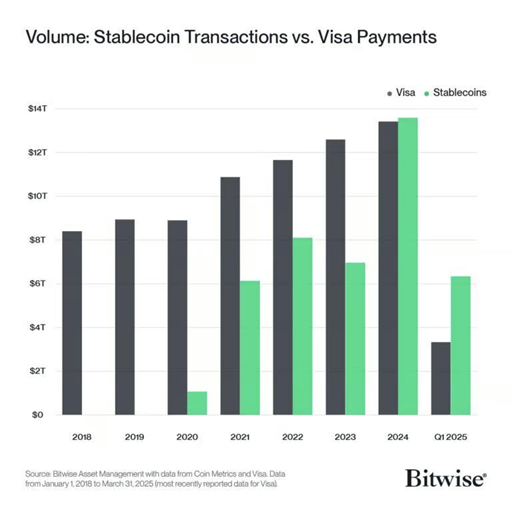

There is a reason why PayPal launched its own stablecoin in 2023, why payments provider Stripe bought stablecoin company Bridge in 2025 and why Circle (the issuer of the second largest stablecoin, USDC), gained 250% in the first three weeks after its IPO. There is an insatiable desire for tradfi to get into stablecoins. We finally have a truly global dollar standard.

From Istanbul to Lagos: why people choose digital dollars

As an advocate of sound money assets, I do not hold a constructive view on the US dollar. The evidence is clear – the dollar has lost immense value, and will almost certainly continue to do so in the years ahead. But the reality is that economics is about relative preferences.

The dollar is far better day-to-day money than most emerging market (EM) currencies. The US dollar has gained almost 400% vs the Turkish lira in the last four years and 270% vs the Nigerian naira in the last three years. Plus, governments in some EMs have imposed onerous restrictions: for example limiting capital flows, restricting offshore accounts and even pulling physical bank notes out of circulation. In these cases, digital bearer assets offer people a way out – faster, cheaper, harder to restrict.

Despite its growing challenges, the dollar is still the global reserve currency, and many more places will accept it as stablecoins proliferate. If you’re settling a foreign invoice or travelling abroad, why pay FX and card fees? Stablecoins are cheaper, faster, digital – and all managed on your smartphone. Despite decades of financial innovation, credit card FX fees still hit 2%- 3%; remittances charge 6% or more.

Source: a16z

Fintech apps, especially in South America, already run on stablecoins in the back-end. In many cases, users don’t even know they’re using crypto. They just see USD – and it works. A 2024 survey from Brevan Howard, Castle Island Ventures and Visa highlights the diverse usages outside of crypto trading.

Source: Castle Island, Brevan Howard, Visa

Safer than bank deposits

Most stablecoins are privately issued, fully reserve-backed. That means tokens are backed one-to-one by assets, usually short- term debt instruments. If the issuer holds those reserves, these are very safe – safer than bank deposits, which are only fractionally backed. There’s still a leap of faith: you’re trusting the issuer, their auditor, or their regulator. The GENIUS Act goes a long way to enshrine this trust – bringing stablecoins under the same standards as traditional money market funds, including bankruptcy remoteness and ring-fenced reserves.

But not all stablecoins are US-regulated. Tether, the largest by market cap, doesn’t fully comply with new US standards yet. And some designs – like Terra Luna’s algorithmic model – are outright risky. Experiments will probably continue but this example serves as a cautionary tale. The market has gravitated towards fully reserve-backed stablecoins for a good reason.

Why governments love (and fear) stablecoins

In America, stablecoins have clearly won the race over Central Bank Digital Currencies (CBDCs). A CBDC would give every citizen an account with the central bank – a powerful tool for fiscal and monetary intervention. But do we want governments this embedded in our financial lives, especially with record debt loads and shrinking trust?

China’s CBDC model is top-down and surveillance-heavy. Europe seems to be following that lead. But the US has taken a different route – favouring private-sector innovation via stablecoins. Not because they’re necessarily libertarian heroes – but because the incentives line up.

Source: Ark

Tether is already one of the largest holders of US Treasuries and the seventh largest buyer in 2024. With stablecoins expected to grow from a $250 billion industry to $2 trillion in the next few years, stablecoins are a critical buyer of US debt at a time when it desperately needs buyers.

US dollar stablecoins dominate global volumes even more than forex, international debt or SWIFT. They give users from Turkey to South Africa an alternative to their national currencies. That makes life harder for EM central banks trying to enforce capital controls. It also entrenches dollar hegemony further than Bretton Woods ever dreamed. Capital flight now moves at the speed of stable- coins. And no central bank can print trust.

Source: Castle Island, Brevan Howard, Visa

But let’s be clear: the dollarisation trend doesn’t mean the dollar is set for a bull run.

The Federal Reserve and Treasury remain committed to debasing the currency - the dollar will almost certainly continue losing value against scarce assets like gold and bitcoin.

Still, stablecoins entrench the dollar’s role as the global reserve unit, even amid growing fragility. Despite serious dedollarisation efforts from China and Russia. Network dominance can survive even as monetary quality decays. And stablecoins are the mechanism through which that paradox plays out.

Stablecoins are the bridge – bitcoin is the destination

For all their benefits, stablecoins are not bitcoin. They gain or lose value in lock- step with the dollar. They are not scarce. They are not permissionless. They are controlled by private companies who can freeze accounts, block transactions, and comply with government pressure. Bitcoin is programmatically scarce, and a far superior long-term investment proposition.

That said, they offer real utility. In countries with capital controls, users may prefer stablecoins to their national currency – and face less censorship risk. But for users in sanctioned regions, even stablecoins will fall short. Bitcoin will remain a lifeline. Nothing can compare to its truly permissionless qualities.

Despite the clear value proposition, many remain resistant to change, and struggle to adopt bitcoin as a result. But what if your only way to avoid 8% fees is to download a crypto wallet? What if the payment provider you utilise globally, like PayPal or Stripe, is using stablecoins on the backend? We expect the regulatory credibility generated from the Genius Act and the numerous touch points created by stablecoin proliferation to further entrench the path to truly decentralised financial technology, like bitcoin. For instance, JP Morgan Chase just linked its credit card rewards to USDC (the second largest stablecoin) on Coinbase – some of this capital will leak from USDC into bitcoin.

Like it, or not, it is inevitable

Stablecoins started as a shadowy workaround – an unlicensed hack stitched onto crypto exchanges. A decade later, they’re issued by PayPal, managed by BlackRock, and endorsed by Congress. That doesn’t make them invincible. But it makes them inevitable.

I don’t like the idea of expanding dollar hegemony – and the US government certainly hasn’t earned it given their fiscal profligacy, but my moral arguments about the dollar amount to nought. The world remains on a dollar reserve standard until such time as we’re ready to move to something different. Bitcoin has put up its hand as a contender but we are so way off the tipping point from the old to the end. Until then, stablecoins are the entry point – the bridge between tradfi and crypto.

And stablecoins are just the beginning. They represent the first wave of a broader tokenisation trend – the movement to bring traditional financial assets like dollars, bonds, and eventually equities onto crypto infrastructure. We expect equities and bond markets to trade 24/7, peer-to- peer, on-chain. Imagine sending an equity in a company to a friend over a messaging app – on a Sunday. That’s where we’re headed. Robinhood, Coinbase and many other exchanges, in both crypto and tradfi, are working to make this a reality.